Time to Nibble? A look at the opportunity in Software

Most investors at this stage are likely aware of, to put it bluntly, the destruction across the software sector. Just two years ago, this was a coveted sector that garnered premium valuations due to the above average, recurring, and consistent growth these companies offered with high margins and typically very strong balance sheets. That all changed when AI burst onto the scene. Business models that were once viewed as defensible were all of a sudden viewed as being at terminal risk with the fear that AI was going to supplant every software service. Over the last year as of May 1, 2026, the software sector represented by the ETF IGV is down 12.9% while the S&P 500 is up 28%. Past software stalwarts such as ServiceNow (NOW) and Constellation Software have seen their P/E valuations compress from the mid 50X to low 20X valuation range and mid-30X to 15X, respectively. This is all while the fundamentals have not really changed a whole lot (yet). But, of course, markets are forward looking and are pricing in what they think will be a material change to these businesses.

We are not here to argue about whether AI is going to supplant software. We have written in the past (https://i2icapital.com/blog/ai-eats-world) that while it will impact some areas and some companies more than others, markets are likely over-extrapolating the real impact it will have on incumbents. Markets often prefer to panic first and ask questions later. We want to look at the situation with a lens of, regardless of AI impacts, does software look attractive at this time?

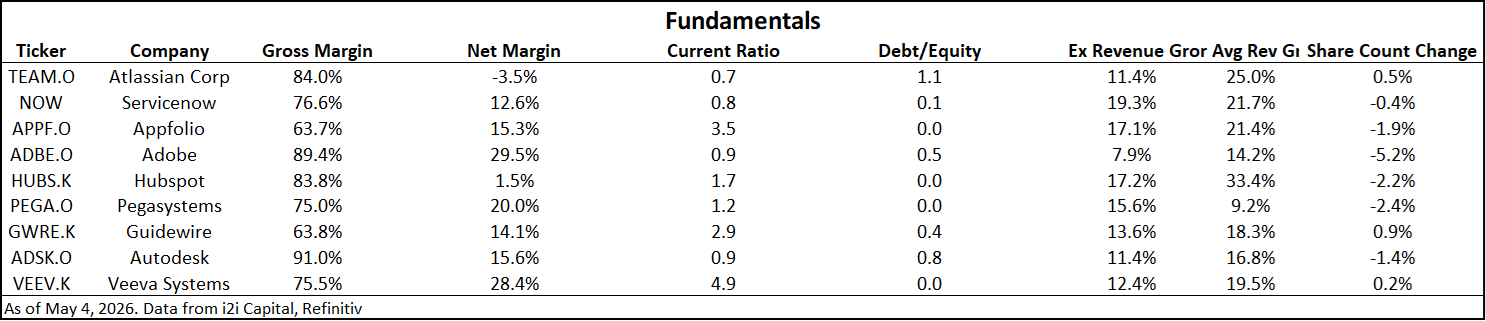

But why now? The sector has seen consistent negative momentum and the slightest negative headlines send most software names down 5%. No one wants to be involved in that! And this is also part of the reason why there is an opportunity. Sentiment is about as bad as it can be. Two primary reasons for why we think now is the time to be seriously sharpening one's pencil is that many names, while still showing some volatility, seem to be finding a floor with their share prices. The other is that positive recent earnings releases appear to be rewarding these companies where in the past they were met with a shrug. We think this might be an early sign that the bottom is in. A final bonus reason is simply that a bit of time has passed for markets to price in the risks, and the valuations are attractive on relative, historical, and absolute levels, creating a bit of a situation where investors might feel a bit silly looking back and not investing at this stage. And as we all know, you don’t get attractive valuations in good times. You get attractive valuations when things seem really bad and risks are staring you in the face. Then, more often than not, the risks don’t become quite what was expected. Below is a bit of a sampling of what we would view as some high-quality software names and some relevant metrics:

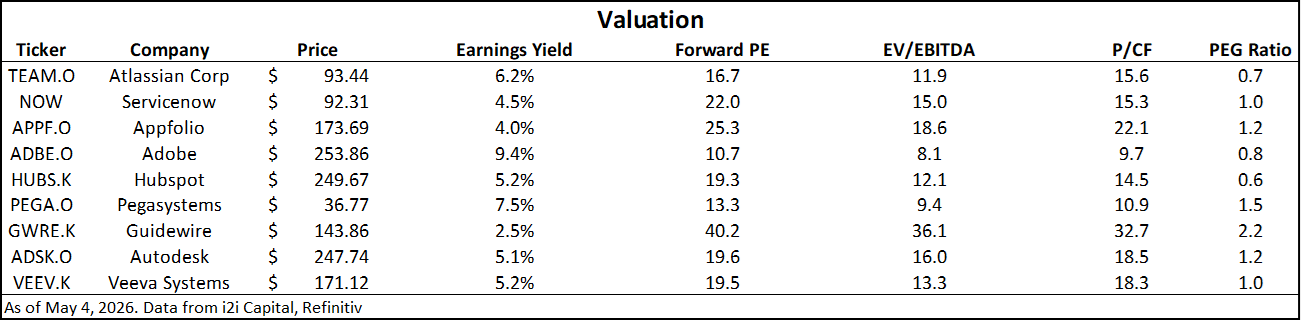

It is a small sampling of names but one that provides a bit of a cross section of what many of these beaten down software names look like. If we were to summarize the above table, we would conclude that software is full of high margin, high growth companies, with strong balance sheets that are repurchasing shares. These are companies that typically trade at valuation premiums. So, what do the valuations look like?

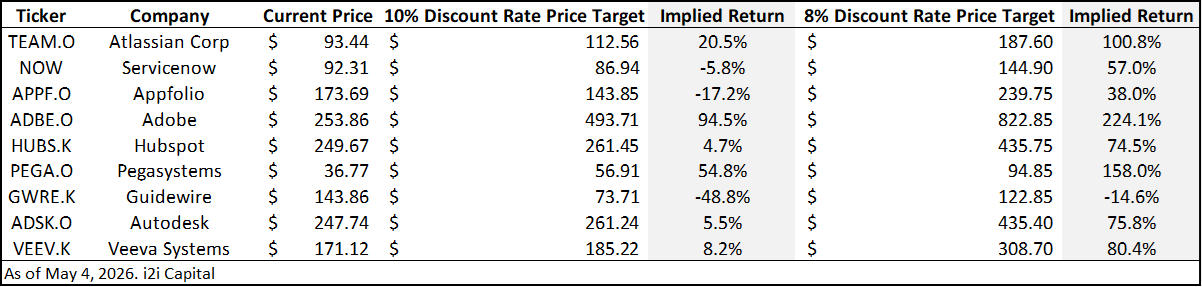

As should be fairly clear, these valuations are not hard to digest whether you are looking at valuations relative to these company’s own history, relative to the market (SPX at ~27X and NDX at ~30X), or even on an absolute basis. While relative valuations look attractive, particularly when overlaying the fundamental backdrop with many of these companies, the issue remains that AI creates a bit of an unknown risk. If AI is truly going to be disruptive, how exactly do you know what a reasonable valuation is? This is of course the entire crux of the issue facing software currently and why markets have decided to just throw everything into the waste basket and come back to it later. On this sentiment alone, you can be a bit more confident that many of these names are likely oversold. With that said, we can do one more round of valuation analysis through some scenario analysis and see what companies should be worth in an ‘AI eats the world’ scenario. For each of these companies, we are going to take current year analyst EPS estimates and assume these are reached but thereafter, we are going to assume growth hits a wall at 5% going forward. 5% growth should be fairly achievable between simple inflation/GDP based growth with a bit of a buyback. Remember, many of these companies have no debt and in theory could repurchase some level of shares for the foreseeable future. So, we think 5% growth is reasonable from a near worst-case type of scenario that reflects potential threats from AI.

As we can see, even if we use a largely unrealistic and very conservative scenario where all of these companies essentially hit a growth wall next year, in most cases there remains very attractive upside opportunities and at worst, limited downside. This is also before taking into consideration any value of cash on these balance sheets. VEEV, for example, has roughly 20% of their market-cap in cash and we are not even bothering to capture these factors in this analysis. While there can be no certainty on the impact AI will have in reality, this scenario analysis gives us a pretty good idea that whatever impact it might have, markets are already pricing in a lot of this impact as a reality already, a conclusion which we view as being very uncertain at this stage.

We won’t go too deep into why markets might be over extrapolating the impact AI will have on software companies, as we dove into the topic earlier (linked in an above paragraph) but we think there have been two framing errors around AI over the last two years. The first is around job losses which we think is the wrong perspective. Investors should be thinking about the opportunity of AI driving economic growth, activity, and job and business creation. The hurdles to start a business of any kind have probably never been lower and more cost effective. The second is how AI and software interact. The narrative has been that AI will simply replace software but the reality, at least so far, appears more that software companies are going to ‘simply’ integrate AI into their platforms, making the current software easier to use and navigate and also being more powerful for the average user. Even if ‘seats’ might fall, there is likely to be an offset through usage pricing for the remaining users. It remains early but it increasingly looks like AI will be additive and cooperative to the incumbent and proven software, not combative.

In the short-term and given the drawdown this space has seen already, patience will likely continue to be the name of the game for software companies. However, with a few recent catalysts, we think it is time to start digging into the opportunities in this space and nibbling ever so slightly at interesting names. Attractive prices don’t tend to appear in ‘good times’ but when a whole sector has been written off and no one has an interest to dig into the space, it is probably a good sign on its own that it is time to dig into things a little!

> > >

i2i Capital has a financial or other interest in HUBS, GWRE, VEEV, TEAM

Forward-looking information contained in this presentation is based on the current estimates, assumptions, expectations and projections, which are believed to be reasonable as of the current date. There is no assurance that these estimates, assumptions, expectations and projections will prove to have been correct. You should not place undue reliance on forward-looking information contained herein. i2i receives no compensation of any kind from any companies that are mentioned in our analysis and commentary or on our website. Any opinions expressed are subject to change without notice. The i2i Fund, employees, writers, clients, and other related parties may hold positions in the securities discussed in these pages, presentations, or on our website. Any information, recommendations, or statements of opinion provided here and throughout the i2i website are for general information purposes only. It is not intended to be personalized investment advice or a solicitation for the purchase or sale of securities. The information contained in this publication are obtained from, or based upon publicly available sources that we believe to be reliable. i2i makes no warranty as to their accuracy or usefulness of the information provided. i2i will not be liable for any losses or liabilities that may be occasioned as a result of the information or commentary provided. Do not buy or sell any security without conducting your own due diligence or consulting an advisor. i2i Capital Management acts as the funds exempt market dealer, portfolio manager, and investment fund manager. Introductions are permitted exclusively through registered exempt market dealers.